We know of Bitcoin and Fintech, but what about Insurtech?

Blockchain and GDPR: Will the new EU data privacy regulation kill blockchain businesses?

How Cooperation can be achieved in Competitive Environments

Crowdfunding for Goods: A caveat

What is wrong with Google’s and Facebook’s tax status: The EU proposal on the taxation of digital…

Blockchain and Negotiable Instruments

It’s a bird … it’s a plane … it’s … an ICO?! Let’s check what their Kryptonite is

Smart Companies: Machines in the Boardroom

How Robo-Advisors Are Disrupting the Wealth Management Industry

Before and After: Reading 100 ICO projects will make you … (fill in applicable…

“I worked with startups and I survived!”

1001 Accelerators — The Tale of the Right Choice

How the Blockchain Technology Could Revolutionise Supply Chain Management

Short History of ICOs: From Crypto Experiment to Revolution in Startup Financing

We know of Bitcoin and Fintech, but what about Insurtech?

Imagine a world where you have full autonomy to decide what you want to be insured for. We would no longer have to worry about overpaying for unnecessary insurance coverage, enjoy a flexible pay-as-you-go insurance system and immediate pay outs for medical bills with a simple tap on your smartphone. This is exactly what is happening with the rise of Insurtechs and their increasing collaboration with traditional insurance companies. In this blog post I share my thoughts and experiences from attending the Digital Insurance Agenda (DIA) which took place in Amsterdam on 16 and 17 May 2018 and how it contributed to my research on Insurtech.

What is Insurtech?

“Insurtechs” are technology-driven companies that utilize new technologies to provide innovative solutions, coverage, and enhance the overall customer experience in the insurance industry. Similar to Fintechs, Insurtechs are spreading innovation throughout all levels of the industry and creating a healthy competitive environment that is seen by some as a threat to the current incumbents and by others as an opportunity to collaborate in a world where new technologies are redefining what it means to be digital.

For instance, smartphone applications, wearable devices, online policy handling, and claims processing tools are all considered Insurtechs which are useful for collecting and analyzing consumer data to provide a better service.[1]

DIA 2018

During this 2-day event, more than 1200 leaders in the field gathered in Amsterdam to share the latest developments in Insurtech and how to successfully (continue to) implement these innovations in the insurance industry. Discussions and presentations stressed the benefits and opportunities of Insurtech for the insurance industry and addressed practical questions such as; the shift from a one size fits all insurance policy to a custom-tailored insurance policy focused on meeting customer’s needs available at their fingertips, and the need for more collaboration between insurance and Insurtech companies. The main recurring themes of the DIA are discussed below:

Building Trust

“We should grow as an ecosystem, too many startups are trying to do things on their own. It is essential that we work together to make insurance more accessible.” — Oskar Melczarek de la Miel (Founder and Managing Partner at Rakuten Capital)

Traditional insurance companies can no longer circumvent the developments in Insurtech. It’s time to step up their game and get with the program. However, at the same time Insurtechs should not be naïve to think that they can singlehandedly take on and disrupt one of the oldest and most trusted industries in the world — insurance. Collaboration is crucial to build a healthy ecosystem that fosters innovation.

Simple, Accessible, Transparent and On Demand Insurance

“Customers want value, trust and choice in insurance” — Tom Van den Brulle (Global Head of Innovation Munich RE)

Customer expectations are higher these days due to engagement and innovations across multiple industries (think Apple, Google, Amazon, Uber, Airbnb). Consumers have adapted to certain industries getting things right, especially when it comes to knowing who we are, what we like and what we need. As consumers have become more accustomed to unique user experiences offered by tech companies they now expect the same from financial services, including but not limited to the banking and insurance sectors.

Know Your Customer (KYC) — Nowadays, it is starting to become all about your individual customer — a shift from the outdated one size fits all insurance coverage. Insurers and Insurtechs must create insurance products and services tailored to the individual’s needs. Personalization and technology does not just mean addressing the consumer by first name and using a Chabot, because the reality is that nowadays everyone is doing this. Customers want to feel like they have a connection with their insurance company, to feel like their individual needs are met and understood. They key, is to build-up a relationship with the customer of trust, confidence and simple access to your product at all times. Therefore, to further enhance the user experience it is essential to provide simplicity, clarity and a clear understanding of their insurance contract and coverage(s).

“Insurance is too far away from the customer; digital companies understand customers better. It is a data game where IoT and wearables generate mass amounts of data — Insurance is a connector.” — Bill Zong (Chief Operating Officer at ZhongAn International)

Being at DIA felt like I was living and breathing all things entrepreneurial and Insurtech related. At the same time, it triggered my academic interest in the issue and I was able to translate developments in the field and upcoming trends into questions that would require further academic research.

Researching Insurtech

Technology is developing faster than regulation — resulting in the need for a solution to regulate the technologies that Insurtechs are using while protecting the consumer. We need to co-create ecosystems that encourage these technologies instead of covering them with red tape. Germany and the UK are just two out of many countries where regulatory barriers have been lowered to encourage insurtechs to test their innovative business plans on specific segments in the insurance industry.[2] The use of regulatory sandboxes is one possible solution as a mechanism to develop regulation that keeps up with the fast pace of innovation in the Insurtech industry. In my Master thesis, I am researching what implications Insurtech has for the current regulatory framework of insurance, particularly in respect of blockchain technology, smart contracts and the internet of things.

Recently, there has been a growing concern that there may be some fundamental incompatibilities between blockchain technology (and it’s many applications) on one hand and the soon to be operational GDPR on the other.[i] For the uninitiated, the GDPR or General Data Protection Regulation is the new EU level data protection legislation, which shall go into force on May 25, 2018. The GDPR applies to all forms of handling “personal data” that is any data pertaining to identifiable individuals. It also recognize individuals’ rights to retain some element of control over what happens to data pertaining to them. Under the GDPR, data controllers are expected to abide by certain principles and data subjects have been granted several rights including the right to know what, why and how data pertaining to them is processed and by whom. For instance, the fact that data subjects have been granted the “right to be forgotten” is often cited as an example of the incompatibly with the “immutable” nature of blockchain.[ii] At the same time, there is a growing belief that blockchain can have several privacy enhancing applications.[iii] This blog seeks to briefly expand on some of the tensions that have been identified as existing in relation to the GDPR and blockchain[iv].

What goes on the blocks? Is it personal data?

The GDPR applies to the processing of personal data by wholly or partly automated means[v] where ‘personal data’ is defined as “any information relating to an identified or identifiable natural person (‘data subject’); an identifiable natural person is one, who can be identified, directly or indirectly, in particular by reference to an identifier such as a name, an identification number, location data, an online identifier or to one or more factors specific to the physical, physiological, genetic, mental, economic, cultural or social identity of that natural person”.[vi]

The easiest way to comply with the GDPR is to simply avoid the application of the law by not processing any personal data, as is the case with handling anonymous data.[vii] However, in practice achieving “true” anonymization is not easy owing to the high threshold of “irreversibly prevent identification” that must be satisfied to meet this claim.[viii] The Working Party 29 has provided an in-depth opinion on the various anonymization techniques which may or may not meet this standard.[ix]

In the context of blockchain, two techniques analyzed by the Working Party are of particular relevance, i.e. Hashing and Encryption[x]. According to the WP29 neither of these techniques achieve anonymization, but are rather methods of pseudonymisation. Since pseudonymisation reduces the linkability of a dataset with the original identity of the data subject, the WP29 considers it a useful security measure but not a method of anonymization.[xi] Therefore, the GDPR continues to apply to pseudonymised data.

With regard to secret key based encryption, the WP’s stand is based on the fact that the re-identification merely requires knowledge of to the correct key.[xii] With regard to hash functions, the WP has this to say:

“Hash function: this corresponds to a function which returns a fixed size output from an input of any size (the input may be a single attribute or a set of attributes) and cannot be reversed; this means that the reversal risk seen with encryption no longer exists. However, if the range of input values the hash function are known they can be replayed through the hash function in order to derive the correct value for a particular record. For instance, if a dataset was pseudonymised by hashing the national identification number, then this can be derived simply by hashing all possible input values and comparing the result with those values in the dataset. Hash functions are usually designed to be relatively fast to compute, and are subject to brute force attacks. Pre-computed tables can also be created to allow for the bulk reversal of a large set of hash values.

The use of a salted-hash function (where a random value, known as the “salt”, is added to the attribute being hashed) can reduce the likelihood of deriving the input value but nevertheless, calculating the original attribute value hidden behind the result of a salted hash function may still be feasible with reasonable means.”[xiii]

Having said that, the WP29 Opinion is only indicative and itself acknowledges that every proposed anonymization technique would have to be analyzed on a case-by-case basis. In light of this discussion, we can conclude that the fact that the data stored on the blocks is hashed or encrypted would not preclude the application of the GDPR.

One technical workaround to this problem is that no personal data should be stored on the blockchain. This can be achieved by storing the personal data off-chain and be merely linked to the blockchain with a hash pointer.[xiv] According to Fink, at present the storage of personal data off chain is the most important solution towards GDPR compliance for blockchain solutions.[xv] Having said that, while this solution may be an effective means of handling “transactional data”, it cannot solve the problem of handling public keys. Fink concludes that public keys are pseudonymous data, which are caught by the GDPR and unlike transactional data cannot be moved off chain as they are quintessential components of the technology.[xvi]

We can conclude that blockchain developers need to be mindful of the distinction between anonymization and pseudonymisation and especially not confuse the former with the latter.

On a blockchain, who does the GDPR apply to?

Assuming that a blockchain solution involves the processing of personal data, who on the blockchain needs to comply with the GDPR obligations?

The GDPR applies to data controllers which are natural or legal persons who “determines the purposes and means of the processing of personal data”[xvii]. While, in the case of private blockchains, it may be possible to identify a central intermediary, which can be termed as the controller for the purposes of the GDPR, the same may prove to be a much greater challenge in permissionless (public) blockchains.[xviii] In such a situation, it can be argued that either no node on the blockchain is the controller or that each node qualifies as a data controller, with the latter being the more likely interpretation adopted.[xix] However, individual nodes on a blockchain have limited abilities to influence the data on a blockchain and are therefore likely to be unable to comply with the obligations placed on data controllers by the GDPR.[xx] Of course, the determination of who controllers and processors of data are, would have to be based on the governance arrangement of each particular solution.

Data subject rights: How to comply on a blockchain?

Article 5 of the GDPR lists the broad principles that a controller has to comply with if it wishes to process personal data. These principles are that data should be processed:

a) in a lawful, fair and transparent manner;

b) collected and processed for a specified purpose and not used beyond those purposes (purpose limitation);

c) only limited data necessary to the purpose be processed (data minimisation);

d) personal data must be accurate and ensure that inaccurate data should be erased or corrected (accuracy);

e) stored no longer than is necessary(storage limitation);

f) ensuring appropriate security measure (integrity and confidentiality).[xxi]

One can easily recognize that some of these principles are fundamentally at odds with blockchain technology. In particular, the fact that data is continuously added to the chain without the possibility of deletion or editing, makes it very difficult to comply with the data minimization, accuracy and storage limitation obligations.[xxii]

The GDPR grants data subjects certain rights with regard to their personal data, which they can invoke against data controllers. We shall now examine how some of these rights interact with personal data stored on a blockchain.

Article 15 of the GDPR grants data subjects the right to ask a controller if personal data pertaining to him is being processed by it and if so, grant him access to such data including the right to receive a copy of such data. In most cases, since the data on the blockchain will be cryptographically pseudonymised, it would not be possible for a controller to confirm or deny to a data subject that data pertaining to him is being processed. The same problem would come in the way of the data subject asking for a copy of the personal data since the same is stored behind encryption. In the case of an unpermissioned blockchain, it would in fact be possible for the data subject to download the entire chain but it is unclear if this would satisfy the GDPR obligations[xxiii]. For instance, what would happen in a situation where a person gets locked out of his data owing to having lost his private key?

Article 16 of the GDPR grants data subjects the right to have inaccurate data about them rectified by the controller. In a similar vein, Article 17 of the GDPR enshrines what has come to be known as the “right to be forgotten” allowing a data subject to seek deletion of his data if certain grounds are met. In the context of the blockchain this raises two issues: would such a request have to be addressed to every node since each is a controller? Secondly, due to the immutable nature of the ledger, nodes may not have the ability to correct the personal data stored on the blocks.[xxiv]

Conclusion

As can be seen from the above discussion, there appear to be some fundamental incompatibilities between blockchain technology and the GDPR. This incapability stems from the fact that the GDPR was designed for centralized data collection, storage and processing and these concepts are difficult to apply to a decentralized blockchains.[xxv] The proposed technical solution of not storing any personal data on the blockchain though appealing, does not completely address the tensions we have identified. For one, it does not provide a solution for the storage of public key. For another, it does not address the fact that someone would still be a controller or processor for the off-chain storage used to store the personal data.

[iv] Blockchain based solutions take many shapes and forms and the actual applicability of the regulation will depend to a large extent to each solution’s design and governance structure. The attempt here is to highlight some tensions with the “general” properties or techniques associated with blockchain.

[vii] Recital 26 GDPR “….The principles of data protection should therefore not apply to anonymous information, namely information which does not relate to an identified or identifiable natural person or to personal data rendered anonymous in such a manner that the data subject is not or no longer identifiable. This Regulation does not therefore concern the processing of such anonymous information, including for statistical or research purposes.”

[viii] Michele Fink, Blockchains and Data Protection in the EU, November 30, 2017, Max Planck Institute for Innovation & Competition Research Paper №18–01. Available at https://ssrn.com/abstract=3080322

How Cooperation can be achieved in Competitive Environments

To cooperate or not to cooperate, that is the question— and the answer from Robert Axelrod’s Evolution of Cooperation

Humankind’s evolution as a superior specie has a lot to do with our high intellect as well as our ability to cooperate. In spite of the primal instinct to hold our interests dear at the expense of others, the positives created by the interdependence and cooperation among our peers often led to the subordination of personal interest for the sake of societal gains. However, cooperation is not easy to sustain considering our egocentric and sometimes sneaky characters. People will always search for ways to maximize their payoffs — sometimes without realizing cooperation has always been the best option for maximization.

Anarchists would like to have a word with you Mr. Hobbes.

According to Hobbes, cooperation could not develop without a central authority, yet there is not a central authority for every aspect of life necessitating cooperation. Ever since, the question of whether a decentralised cooperation can emerge was challenged with a separate field of mathematics, game theory.

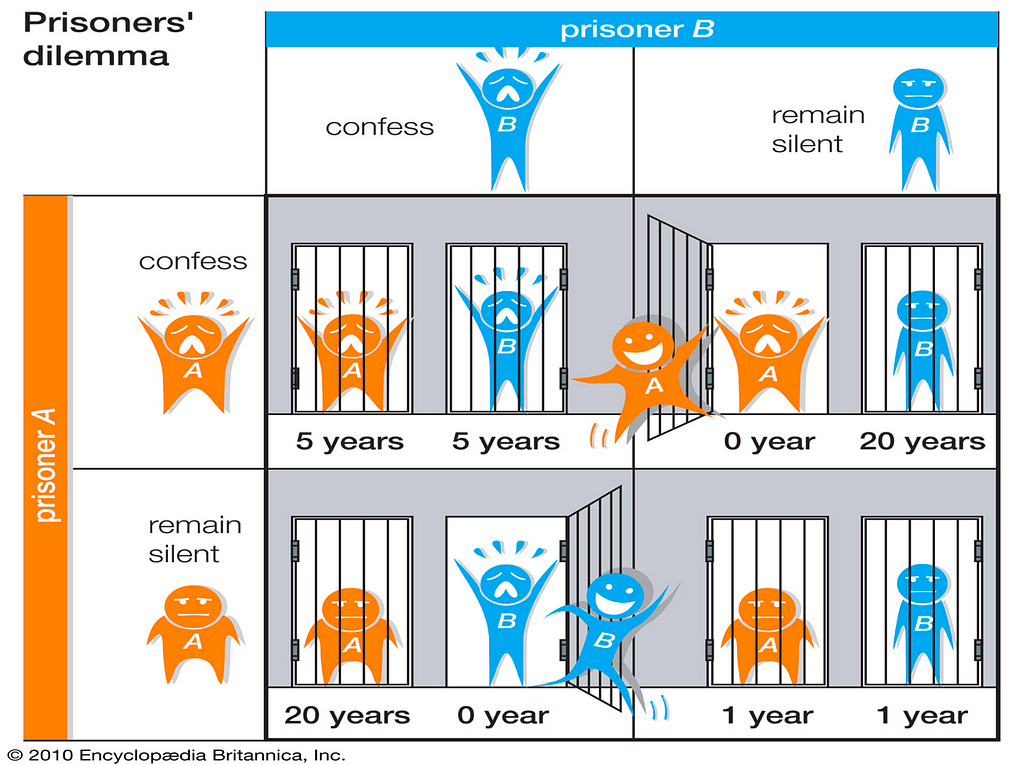

There are millions of scenarios where pursuit of self-interest leads to a poorer outcome for that person as well as for the others in comparison with cooperation. A famous representation of such scenarios is the Prisoner’s Dilemma game.

The game goes as follows: There are two prisoners who are interrogated separately but simultaneously. Interrogators offer both prisoners two options: confess their counterpart’s involvement in alleged crime or remain silent. If prisoners cooperate with one another and remain silent they will both receive 1 year of imprisonment. If one of them bails out and other remains silent, the snitch will be released whereas the silent prisoner will receive 20 years. If both of them bails out on one another, they will both receive 5 years. You, as Prisoner 1, are asked to decide.

Prioritising your self-interest without considering what happens to Prisoner 2, there are two possible actions your counterpart may take which you have to consider to develop your own strategy. If you believe that Prisoner 2 will remain silent, it seems better for you to confess his crime as you will be released whereas if you also remain silent, you will stay in prison for a year. Similarly, if you believe Prisoner 2 will bail on you, again it seems better to bail on him since you will receive only 5 years, whereas if you remain silent your punishment will be 20 years. So, no matter what Prisoner 2 does, you should confess his crimes, right? Not really. The flaw of this logic comes from the disregarding the logic of Prisoner 2, who would also think he should confess on your crimes no matter what you will do. As a result, you will both bail on one another and receive 5 years, whereas if you both cooperated and remained silent punishment would be only 1 year. In this case individual rationality leads to a worse outcome for both than is possible. Hence the dilemma.

How to determine the best strategy for multiple sequences of Prisoner Dilemma?

Prisoner Dilemmas, although not in literal sense, are everywhere in our daily and professional lives. In core, every scenario where there is lack of pre-settled trust and personal interests of two parties partially collide with one another has the same dilemma: A business relationship, or even a romantic affair can be subjected to it; however, in real-life there usually is not only one sequence of decision-making — there are many of them for the same example.

To put things into context, let’s give a more real-life like example to the Prisoner Dilemma. Assume that you and your housemate has decided to determine the payment of your monthly Netflix subscription with a game. Each month, both of you simultaneously put an envelope on the table, after which both envelopes will be opened. You may put inside the envelope a) the total monthly amount of the subscription fee b) nothing.

What’s next: Netflix’s response to HBO, Game of Theories

If both of you chose a, then each of you will receive the half of your money back and subscription fee will be paid. If one of you chose a and the other chose b, the subscription fee will be paid solely by the chooser of a and chooser of b will enjoy a month of Netflix for free. Lastly, if both of you chose b, subscription fee will not be paid and you will be doomed with the lack of Netflix & Chills for an entire month. Same logic as Prisoner Dilemma, however as you can realise this game will take place every month, and over the course of months you will get to learn if your housemate is a horrible person who never pays or someone with deep pockets who is happy to sponsor your Netflix & Chill sessions — and vice versa.

Determining a “best strategy” requires the mention of some ground rules. First off, it cannot be considered separately from the other player’s strategy. Second, the pessimistical assumption of the other player making the feared move will lead to you making the same move as well, causing mutual punishment. A chess player can safely use this assumption as it provides the ability to foresee your opponent’s move in a game like chess, where players’ interests are in total conflict — there cannot be two winners or two losers. On the contrary, situations represented by the Prisoner’s Dilemma game have personal interests that are not in total conflict as mutual cooperation is rewarding.

The winningest strategy: TIT FOR TAT

To find out the best strategy, a multiple sequence Prisoner Dilemma tournament was organised with participants submitting their favorite strategy, and the winner was surprisingly the simplest of all strategies submitted: TIT FOR TAT, the strategy which cooperates on the first move and then mirrors the other player’s previous move.

There are four main attributes of TIT FOR TAT behind its success:

• “avoidance of unnecessary conflict by cooperating as long as the other player does,

• provocability in the face of an uncalled for defection by the other,

• forgiveness after responding to a provocation,

• clarity of behavior so that the other player can adapt to your pattern of action.”

The unique combination of being nice, retaliatory, forgiving, and clear balances the weaknesses of each attribute: Niceness prevents unnecessary trouble while retaliation discourages the other side from resisting not to cooperate. Forgiveness allows to restore mutual cooperation while the clarity offers intelligibility and transparency to the other player, thereby eliciting long-term cooperation.

Some life lessons

21st century people, while functioning as a society under a social contract, has embraced the ideals of individualism and self-determination of one’s true potential. We tend to think that if everyone pursues their own interest, this competition will lead to the most efficient and collectively-rewarding result — this is how Adam Smith envisioned it back in the day. Yet, thanks to the game theory we now have discovered a third way: cooperative competition (or competitive cooperation). This offers us to get the best result for ourselves as well as for the others, and unlike the sole pursuance of self-interest, with more people acting in the same manner this strategy’s personal outcome can only get better.

Levent Aslan, Social Media Guy

Crowdfunding for Goods: A caveat

Source: Makezine

Traditional financing has taken a back seat over the course of the last few years with alternatives offering unique and sometimes legally-challenging opportunities to raise capital without the classic intermediary of regulated banks or capital markets. Initial coin offerings and peer-to-peer consumer & business lending are couple of examples need to be mentioned as well as the crowdfunding, practice of raising money from a large number of people through unconventional intermediaries typically using the Internet infrastructure.

Earlier this year, Luton County Court ruled that a transaction made on one such unconventional intermediary, Indiegogo, gave rise to a contract of sale between the parties of Morton v Retro Computers Ltd case. The case started after the defendant, being “donated” money to its crowdfunding campaign to produce the Sinclair ZX Spectrum Vega Plus by the claimant, failed to deliver the product long after the campaigns’ closure.

In the court’s reasoning it is indicated that there was in fact a contract of sale that arose from the transaction. According to the judge, documentation carried importance as its language could give rise to a contract — it stated that “this order” had been added to the campaign, not “this pledge”. It is this initial phrase which gives rise to the contract in some certain terms, between the two parties without taking into account the position of Indiegogo as the intermediary.

The judge also found that the terms and conditions for using Indiegogo did not negate the existence of a contract of sale, and within the terms it was stated that “campaign owners are legally bound to perform on any promise to contributors, including delivering any perks”; which arguably strengthens the existence of a contract within these circumstances.

Some regard this as the breakthrough case; however it has not set any binding precedent given it was only a dispute in the County Courts. The judgement however gives some indication as to the considerations that will be important for the court. My interpretation of the judgement is that the framing of the crowdfunding campaign will be a deciding factor within future judgements, and that the courts will look at the language and phrases used by the company to help ascertain this fact. The other core aspect that the courts probably would have to look at is the terms and conditions of the intermediaries who facilitate crowdfunding; and much like Indiegogo did not seek to negate the potential inference of a contact.

However in many respects I would argue that when looking at the broader circumstances of Contract law in the UK, a variety of issues arise. The first matter is that of contractual certainty; in the case of G. Scammell and Nephew, Limited v H.C and J.G Ouston [1941] A.C 251 it was stated that if there was even a clause that was too vague no precise meaning could be attributed to it, there would be no enforceable contract between the parties. When looking at most crowdfunding campaigns in light of this case, the actual scope of the product and delivery of it could be the elements which are vague enough to defeat the concrete conclusion of the contract, though in the circumstances of the Retro Computers case this would not have been an issue given that they actually provided an expected date for delivery.

Another matter is as to whether there is a sufficient consideration from the company in offering a product that has yet to be made; this issue is exacerbated by the fact that some crowdfunded projects start when they are initially just a concept with no tangible product to show and offer, such as various video game crowdfunding projects. This issue also ties into the issue set out in the above in regards to the vagueness of terms which would prevent the completion of the contract.

Another concern would be whether to enforce the contractual performance to meet arbitrary deadlines would be too onerous to the companies seeking to drum up interest and funds to allow them to continue working on the product. The contract coming into existence under these circumstances places constraints as to when they are expected to deliver, especially when a company is constantly updating the backers, so they know what is going on with the project they have backed.

The actual legal position of “Reward Crowdfunding” has yet to be determined in the definitive limits of the law; the benefits of this case is that it gives us insight into the matters the court will consider when determining whether a contract and the connected obligations exist. This is an area that should be followed closely, for when such an issue arises again in the courts, the question that should be asked is whether such a case could reach the court of appeal and their judgement could have the potential to send shockwaves if they confirm the opinions at this first instance trial.

Though for now, both parties should be aware that a risk exists for them in reward crowdfunding. Backers should be aware of the old adage “Caveat emptor” and not be to reliant on the protections offered by contract or consumer protection law; while companies engaging in this type of crowdfunding should be cautious and acknowledge that they may be hit by obligations from virtually nowhere.

Matthew Quigley, Guest Blogger

What is wrong with Google’s and Facebook’s tax status: The EU proposal on the taxation of digital…

What is wrong with Google’s and Facebook’s tax status: The EU proposal on the taxation of digital economy

Do you know that it took radio 38 years to reach the audience of 50 million and that the mobile application Pokemon Go did the same in …10 days? Every day we read about new success stories of online platforms, which were fast at growing their user base and pushing competitors aside. Although digital start-ups are diverse in nature and countless in numbers, business models of many of the online or mobile P2P, B2B and B2C platforms include commercialization of their subscribers’ base and generated data (content). The unravelling story of Facebook users’ data being inappropriately used by Cambridge Analytica in targeted election advertising is only one example of such focus on user-generated data. Of course, this business model is very controversial from the perspective of data privacy and security, but what about taxation? How, and most importantly, where to tax the online platform, the profit of which is generated from the user base and content? This article outlines recent developments in digital services taxation at the European Union level.

Digital Services Tax Directive Proposal

There is currently no specific pan-European taxation of the digital economy. However, European legislators cannot but acknowledge the rising trend of the Member States to unilaterally impose digital taxation on such giants as Google. Countries such as Italy and Hungary impose indirect taxes on digital services and by doing so may pose a threat to the internal market. For this reason, the European Commission drafted and on 21 March 2018 published the draft Proposal for a Council Directive on the common system of a digital service tax on revenues resulting from the provision of certain digital services (Digital Services Tax Directive Proposal (DST Proposal)).[1]

Which digital activities are subject to the proposed tax?

Introduction of the digital services tax (DST) is a temporary measure that, if approved by 28 EU Member States, will allow taxing the following types of digital activities:

1. the placing on an online platform of advertising targeted at users of that platform (“Advertising Services”);

2. making available a multi-sided online platform, which allows users to find other users and to interact with them, and which may also facilitate the provision of underlying supplies of goods or services directly between users (“Intermediary Services”);

3. the transmission of data collected about users and generated from users’ activities on online platforms (“Transmission of User-Generated Data”).

By definition, Advertising Services and Transmission of User-Generated Data are taxed regardless of the characteristics of the online platform, while Intermediary Services only concern online platforms, which allow horizontal search and interaction between users and / or exchange of goods or services. So, for example, the provider of the digital content Netflix will not perform Intermediary Services because the core of the service is not based on interaction between users and does not include a horizontal search feature. It is not per se platform such as Facebook or Twitter. The mobile messenger Telegram and the photo and video sharing application Instagram will also not qualify as Intermediary Services — their users pay no subscription fees and the main purpose of the apps is to enable communication. However, in the case of Instagram, placement of advertisement on the platform will be recognized as Advertising Services (Telegram does not host advertisements) and depending on who ordered the advertisement (advertising agency or business customer directly) the payer of the tax on digital services will be either Instagram or the agency.

Place of taxation

According to the DST Proposal, the value of online platforms is created by users and the user-generated content. That is why the place of taxation is determined by reference to the location of the user of the platform or, more specifically, to the location where the device was used to access the online platform at the time digital services were performed. The device, in its turn, is localized by its IP-address.

Rate

The proposed tax rate is 3% of gross receipts from the sale of digital services (excluding other taxes paid on that amount).

Who is subject to the proposed tax?

The digital service tax does only target such giants as facebook, google, ebay because of the high threshold of group revenues which is required to trigger taxation (worldwide group revenue must exceed EUR 750 000 000 and total revenue in EU must exceed EUR 50 000 000).

Next steps

The outline of the Digital Services Tax Directive Proposal presented above can be viewed as a common intention of the European Union Member States to introduce a level playing field in taxation of traditional and digital services and to tax profits at the place where the value is created, that is where the users of online platforms are located. It remains to be seen whether this tax will be unanimously approved by the Member States. If not, analogous equalization taxes will continue to be unilaterally introduced in different Members States inspired by the pioneering efforts of Hungary and Italy. This interesting development in the taxation field shows that the manner, in which digital products and services create value has not been completely understood and regulators need to make further steps to make their taxation fair in order to create level-playing field for all products and services.

Can the youngster help an elderly become “hip” again?

I have a dream…

Throughout our history as humankind, we constantly thrived for new technologies to make our lives more developed and efficient. We created technologies that redefine the ecosystems they were built for, and sometimes even redefine the centuries they were built in. The end of 20th century and the very beginning of 21st century were defined by Internet, with its various applications transforming different aspects of certain fields like finance, media, business etc. With a new technology, Blockchain, becoming a serious candidate to define the rest of the 21st century, there are extensive debates and researches over its applications. Smart contract is one such example in the legal field, yet “LegalTech” has the potential to widen even further and become mainstream in law. Transformation and modernisation of law has been relatively slow-paced comparing to other fields; however, constructing new applications of technologies such as Blockchain that will reform and develop the way we perceive and practice law shall accelerate the process and ensure the relevance of law and its experts.

Let’s get legal, me love the legal terminology

The Commercial Law structure varies in different legal systems, though in general certain instruments are common such as the “negotiable instruments”, which are defined as “documents that contain a guarantee or promise to pay a specific amount of money to a person or entity in possession of the instrument, whether on a specified date or on demand”. Main principles and attributes of negotiable instruments — with minor changes — have been the same since its birth. Regulated under Article 3 of Uniform Commercial Code in the US, and under Directive 2014/65/EU and Regulation 600/2014 in the EU, negotiable instruments have multiple functions: they are substitutes for money and regarded by some as “currency substitutes”, while also acting as a credit device with certain forms extending credit from one party to another, and keeping records that are used for financial statements and tax returns.

A famous definition of negotiable instruments given in an English case back in 19th century exhibits their main characteristics: “where an instrument is by the custom of trade transferable like cash, by delivery, and is also capable of being sued upon by the person holding it, it is entitled to the name of a negotiable instrument, and the property in it passes to a transferee who has taken it for value and in good faith”. In other words, negotiable instruments are transferred by delivery, the transferee can enforce rights he/she is entitled to, and, in case of being a bonafide holder, can even acquire a better title — thus, better rights — than the transferor.

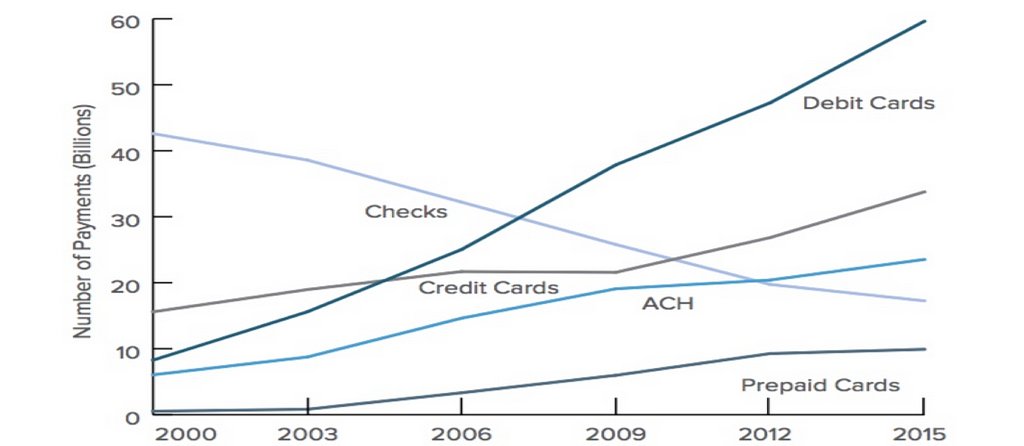

If you want statistics, we have plenty

Trends in Non-Cash Retail Payments by Number and Type of Transaction in USA

Data regarding payments with one of the most commonly used negotiable instrument, check, shows a significant decline in different jurisdictions. In USA, total commercial checks paid decreased by number 3.1 percent a year between 2012 and 2015 to 17.9 billion. In comparison, automated clearing house (ACH) network payments increased by number 4.9 percent to 19.3 billion while card payments increased by number 7.5 percent to a whopping 103.5 billion.

One should bear in mind the fact that USA market uses checks much more than the rest of the world — more than half of business-to-business payments are still made by checks and Americans made, on average, 38 check transactions annually, whereas the number is 18 for Canada, 8 for UK and almost zero for Germany. There are even more extreme examples, with Finland stopping issuance of checks in 1993, Netherlands in 2002 and Denmark in 2017. France, on the other hand, abnormally accounted for 71 percent of all EU checks alone in 2013.

This is the current state of the relationship negotiable instruments have with other payment systems

So, how to make negotiable instruments “great” again?

Common theme in banking industry on checks is that their survival, along with other negotiable instruments, depends on their structural and legal reformation. Currently there are different “value transfer system” alternatives, like automated clearing house (ACH) networks and wire transfers that take place in electronic ecosystems. Without any aforementioned reformation, current negotiable instrument legislation will become irrelevant; yet, with each of these alternative systems being subjected to different codes, acts and/or regulations there is legal complexity and thus, ambiguity. Structurally, there is also room for improvement: A 2014 Federal Reserve study found that “at least 29 billion transactions, or 12 percent of all U.S. payments annually, could benefit from faster authorization, clearing, settlement and/or availability of funds”; meaning beyond negotiable instruments the entirety of current payment system is in need of structural advancement.

Buckminster Fuller once said: “You never change things by fighting the existing reality. To change something, build a new model that makes the existing model obsolete”. The inevitable digitalisation of law means that negotiable instruments will have to adapt and go through a comprehensive reform, or follow Fuller’s advice and through an overhaul to sustain its relevancy. A question would be whether Blockchain technology can be used as the infrastructure for such reformation, especially with its seemingly compatible attributes. Blockchain, as a new “value exchange” network, can offer what current models of negotiable instruments and its more modern substitutes do while adding new features and improving the existing ones. However, with each new (potentially) disruptive technology also comes new (potential) problems to deal with, one of them being the regulatory response to applications using Blockchain.

A last word — and an ice cream viral

My favourite ice cream flavour (not sure about my favourite regulatory authority)

Mougayar humorously compares the variety of financial services regulatory authorities around the world to the number of ice cream flavour varieties, stating “more than 200 regulatory bodies exist in 150 countries, and many of them have been eyeing the blockchain and pondering regulatory updates pertaining to it”. A harmonized response thus seems hard to achieve, especially with private parties taking initiative in Blockchain technology to create applications with different attributes for different industries. Yet, as an existing “application” that is currently regulated by the authorities, modernisation of negotiable instruments through Blockchain can be a two-way street: in addition to the reformation of them leading to the regaining of relevancy, this can also become a pioneer example on how to regulate Blockchain and its applications.

Levent Aslan, Social Media Guy

It’s a bird … it’s a plane … it’s … an ICO?! Let’s check what their Kryptonite is

Source: Bitcoin Magazine

Initial CoinOfferings have just a few years back been an unknown in the investment landscape. They were introduced to the wider public by a panelist at the San Jose Bitcoin conference named J. R. Willet, who had an idea to start a new protocol layer on top of Bitcoin. With this began the (short but exciting) journey of ICOs — basically recorded on an amateur YouTube video that by writing of this blog surprisingly still has (believe it or not) only 476 views.

Since then the rise of ICOs has been exponential, but with their growth many of their vulnerabilities have started to show and the unregulated investment landscape has sadly attracted a fair share of fraudsters.

Some statistics to put things into perspective

According to the tracking website Coinschedule there has been 210 ICOs launched in 2017 raising around $3.9 billion. This number has already been surpassed in the first three months of 2018, as there were already 153 ICOs launched with about $4.9 billion raised. Therefore, not only is there a big increase in the projects launched in comparison with the previous year, but they are also increasing in size.

It is said that during the first two months of 2018 $1.36 billion worth of cryptocurrencies have been stolen by fraudsters through virtual currency scams, hacking attempts, theft, exit scams and phishing. This number also includes the top three scams (Coincheck, Bitconnect and Bitgrail), therefore if those would be excluded, the amount of money lost in first two months would represent $542 million. This means that in average $9 million are lost per day and at this rate the money lost in 2018 will be the double of the GDP of San Marino (for 2017 the estimate of their GDP measured by IMF was $1.6 billion).

I am not stating that every ICO is a scam, namely many these crypto startups are legitimate with a genuine motivation to succeed and to bring their business idea to life. However, statistics show that many of them are being done by fraudulent ventures, and according to a research from December 2017 by Ernst & Young, more than 10% of funds raised last year through ICOs were lost or stolen in hacker attacks. Additionally, according to the website bitcoin.com, 46 per cent of businesses that held ICOs last year have already been unsuccessful.

Worried yet?

The A-List ICOs

Floyd Mayweather, DJ Khaled, Paris Hilton, Jamie Foxx, the Game, Steven Seagal…

You probably heard about them, but what do they have in common?

Well, they were all promoting different ICOs through their social media postings and tried to motivate their followers to invest into them. Seems like a purely philanthropic move from the rich and famous, right? Not exactly, as they all had ulterior motives and received money for this promotion, which they did not disclose. Luckily the SEC stepped in and issued a Public Statement saying that such payment for promotion must be publicly disclosed and a failure to do so would mean a violation of the anti-touting provisions of the federal securities laws. But based on the news that just last week the boxer Manny Pacquiao decided to promote an ICO, it seems that the SEC will need to take a step further to put an end to future celebrity A-List ICOs.

Example of two ICOs that ultimately proved to be a wolf in sheep’s clothing

One of the biggest news of the beginning of the year was the crash of BitConnect, a lending and exchange platform which at its peak had a market capitalization of more than $2.6 billion and their token on exchange was valued at around $430. BitConnect worked as a Ponzi scheme, namely investors who invested their money as a lending amount were offered earnings up to 40% per month. By this, BitConnect attracted more and more investors to back their unsustainable projects, which worked similar to a pyramid scheme. Until it all collapsed in January 2018 when only desperate investors who lost everything were left in the ruins of what Bitconnect once was.

Second equally interesting story is the ICO of OneCoin, which was due on 27 October 2017, but never seen the light of day. The Bulgarian authorities have made a raid at the company’s seat, however the founder — Ruja Ignatova (named the Bulgarian ‘’Crypto Queen’’), and all the leading people behind OneCoin went into hiding, leaving their investors with nothing.

Under some sources more than $300 million has been raised by 3 million investors and then transmitted through dozens of companies in tax havens. While the raid by the Bulgarian authorities may have been the last nail in the coffin of OneCoin, it also provided the perfect excuse for the company, namely the company representatives wrote in a public statement that because of this raid a great financial loss was caused and as a consequence the company may just have to file for bankruptcy. Basically, presenting themselves to be the victim of it all.

Conclusion

Based on all the facts presented above I would like to add once more the continuously repeated statement: ’’Never invest more than you are willing to lose.’’ As any other investment so should an investment into an ICO come with a sufficient amount of due diligence and research in order to avoid losing money.

Important is to check if the token’s developers are anonymous or otherwise-unknown, if the token does not have a clear use case and if the whitepaper sets unrealistic goals — these three basic characteristics are all clear signs that it is a great possibility that the ICO is a scam.

Last but not least: when the team behind the ICO looks like this, it might be good to think again before investing.

Jesus Coin — Team

Source: jesuscoin.network

There is no limit if logic.

Source: reddit.com

The graphic designerKevin Belanger might catch your attention.

In Netflix’s cyberpunk series Altered Carbon, an artificial intelligence personality called Poe is running a hotel, pre-designed to please the guests at any cost. While for now, this is only figment of our imagination and a part of science fiction narrative, it may not be such a distance future.

Last year, in a worldwide survey conducted by Dell Technologies, 3,800 business leaders were asked about how the business world will change during the next decade. 96% of the respondents answered positively on whether companies will automate many of their tasks, many of them falling in the managerial and administrative scope.

Platforms, data and algorithms have already transformed the structure of business. Companies like Uber or Airbnb are already essentially ran by an application, self-driving cars are introduced on to the streets, the Internet of Things enables our devises to communicate with each other and use of robo-advisors is increasing in the financial sector.

But how far are we from the scenario — or for some from the dystopian future — of an algorithm having a position on the board or even owning a company?

One year before this report, Deep Knowledge Ventures, a Hong Kong based Venture Capital firm, appointed — even quasi — an algorithm to its board, granting it the possibility to vote, becoming the first company to do so. The algorithm VITAL made investment recommendations and it was granted the possibility to vote on whether the specialized in regenerative medicine company would make an investment or not.

In 2016, Tieto, a Finnish software company, became the first European company to appoint a bot, named Alicia T, to its management team also with the authority to vote.

How will AI change business management?

AI and machine learning are still immature, but they are evolving rapidly, while becoming more accurate.

AI is already used by innovative companies to offer a more tailor-made experience to their consumers by analyzing their preferences or immediately replying to their questions through bots. This allows them to provide better services or products, on a direct, fast, and inexpensive manner, making these companies more competitive.

By letting AI in the boardroom, tedious and time consuming administrative tasks, like monitoring and reporting, will be off the managers’ hands, allowing them to focus on more important business aspects, such as the company’s future strategy.

As for the important business decisions, for instance whether a merger or an investment should take place, AI, instantly analyzing a plethora of data, will suggest the optimal decision, while considering the relevant regulation.

The trust in a human-machine collaboration was showcased in a recent survey by Accenture Institute for High Performance. 78% of the managers questioned answered positively on whether they will trust suggestions or advices given by intelligent systems when making a business decision.

The Trouble with AI

As with any human creation, the problem with AI lies with the will of its creator. As Elon Musk says in Werner Herzog’s documentary Lo and Behold: Reveries of the Connected World; “if you were a hedge fund or a private equity fund and you said, all I want my AI to do is maximize the value of my portfolio, then the AI could decide, the best way to do that is to short consumer stocks, go long defense stocks and start a war”. For that reason, a paradigm shift in corporate governance is necessary.

At the same time, many fear the unpredictability of AI’s decisions. But is there an actual problem with the unforeseeability of the decisions made by an intelligent machine? And how do those decisions differ from a human’s decision-making process? In the widely praised book Homo Deus, writer Yuvan Noah Harari explains that our own decisions, are utterly random, a combination of predetermined biochemical events and subatomic accidents. And most of the time we will make these random decisions based on incomplete, incorrect and emotionally biased information.

The possibility of an AI facilitating the decision-making process or being appointed with the authority to vote on the board has a law-relevance. First, if AI is used to make suggestions which are subsequently adopted by the board who will be held liable? Is the business judgement rule as a safe-harbor and a standard of care sufficient enough for an “enhanced” manager? And will a type of personhood be granted to the AI to be appointed and able to vote?

As for the latter, on the 2016 European Parliament resolution with recommendations to the Commission on Civil Law Rules on Robotics, a suggestion was made for considering granting in the future an electronic personality to robots — the embodied version of AI — “when they make smart autonomous decisions or interact with third parties independently”.

Managerial Qualities Revisited

Although we cannot predict whether robo-directors will substitute humans in boardroom, managers should still be prepared for the automation era and companies should try to remain relevant.

· Start using AI: In the age where competition is driven by technology and innovation, integrating the plethora of new emerging technologies, including AI, is pivotal for a company to show its adaptability and relevancy to the modern needs of the market, to flourish on the short-term and to survive on the mid- and long-term.

· Appointing an AI Officer: In the Dell Technologies survey 76% of the respondents advised in favor of appointing a Chief AI Officer delegated to oversee the human-machine collaboration. Moreover, an AI Officer can help training and educating the management team about AI, while paying attention to future developments in the field.

· Creative thinking: In the abovementioned Accenture Institute of High Performance survey, 33% of the managers surveyed believe that for a manager to be successful in the future, creative thinking and experimentation are necessary. As AI can be more efficient in analyzing data and information, improvisation, and managerial experience will become of outmost importance.

· Social skills: As the machine takes over many of the administrative tasks, the managers will have to do what the machine cannot. Empathy and social intelligence will bring the human touch in the decisions-making process, while they will enable the collaboration between the board members and the stakeholders.

Conclusion

AI will not necessarily remove human directors, but it will definitely change the character and the dynamics of their work tasks. Directors will very likely become more focused on creativity and new strategies for their business, freeing their minds from repetitive and administrative type of work.

Iakovina Kindlyidi, Guest Blogger

How Robo-Advisors Are Disrupting the Wealth Management Industry

In the last few years many industries have seen their traditional business models being disrupted by startup companies making use of new emerging technologies, such as blockchain or artificial intelligence, to better capture the consumers’ needs. One of these industries has been the financial industry. The intersection between financial services and technology is generally referred to as FinTech and touches upon all traditional services, from payment services to decentralized lending platforms. Among others the financial industry has seen a rise of so called robo-advisors. Growth in the robo-advisory industry has been significant in the last years, especially in the U.S., but Europe is also seeing more and more companies gain market share and expanding across state borders.

What are robo-advisors and what do they do?

The term “robo-advisor” is composed of two separate terms, “robo” and “advisor”. “Robo”, derived from the term robot, refers to an automated process, meaning without any human action, and “advisor” to the service provided by professional advisors. Basically, robo-advisors are digital platforms that provide automated, algorithm-driven financial planning services with little to no human supervision. The term “robo-advisor” is currently mostly used in the context of financial investment advisory, although other industries such as the insurance, health care or real estate industry are also increasingly affected.

The first step in the advisory process is getting to know the potential customer and identifying his risk profile. Since robo-advisors provide their services online, either via their websites or their mobile phone applications, with no human interaction between the advisor and the client, the assessment of the client’s risk profile happens online as well. The process is similar for all robo-advisors; when signing up with a robo-advisor, the client is asked to fill out an online questionnaire, in order for the robo-advisory company to be able to make a profile of its customer and build an understanding of what the client seeks with their investments. Based on this profile, the robo-advisor would then start to make specific investment recommendations.

Robo-advisors predominantly invest in products that require no or less active portfolio management such as exchange traded funds (ETFs). ETFs are funds that track indexes like the NASDAQ-100 Index, S&P 500, Dow Jones, etc. By simply matching and not trying to outperform the market, they do not need active management, which makes them inexpensive to run. Additionally, they are interesting as they allow investors to invest in a diversified portfolio, so they are less affected by single-security price changes.

Their target customer

Over the past years, financial innovation has presented investors with an increasing number of different financial options making financial decision making ever more complex. Investing is complex because, in addition to understanding the financial markets and the ever widening number of different available products, investors must be able to among others evaluate risk and understand tax implications. As a consequence, investors with low financial literacy are particularly likely to make poor financial decisions. That is why these financial non-literate are the main target customers of financial advisors.

Within this group of investors with low financial literacy, there are those that do not own enough money to go to a traditional financial advisor or those who are simply too cost sensitive to pay for their services. Indeed, robo-advisors often appeal to less-wealthy investors, given the availability of low-minimum and low-cost portfolios. The average size of a robo-advisor account is between $20,000 and $100,000, suggesting that the greatest traction has been achieved amongst the mass market and mass affluent demographics. With banks increasingly downsizing advisory services especially for less-wealthy investors, robo-advisory services are becoming the only way for these people to participate in financial investment.

Additionally, robo-advisors’ target customer would encompass all those people who have a certain distrust in the traditional financial institutions, especially since the financial crisis of 2008, but nevertheless want to save money and invest to see their wealth grow. By being fully transparent on their fees and by letting their clients to some extend individualize their portfolio, robo-advisors still let their customers feel like they are being empowered and in control.

How are they disrupting the industry?

As already mentioned, robo-advisors’ main selling point and advantage over traditional financial advisors, is their comparatively lower fees. Traditional wealth managers charge in general more than 3% of their clients’ portfolios every year, even when there are few changes to the portfolio outside of occasional rebalancing of assets. When robo-advisors provide similar services they will generally fix their price at less than 1% of the invested amount.

These lower fees have their roots in the online nature of robo-advisors’ services. Traditionally, financial advisors have to sign scanned papers and even meet the client in person. This takes up much time and sets a limit on how many customers could be served by one wealth manager and at the same time is also very expensive for the advisor. By providing most of the interaction online, robo-advisors can save time and costs. Indeed, the provisioning of the whole service via an online platform additionally reduces personnel and asset costs while a higher number of customers can be served. At the same time, the low complexity of these products makes them easier to explain to a wide range of customers.

The opportunities are non-negligible and more and more startups are entering the wealth management industry with this new business model, gaining market shares at an astonishing quick rate. In the US, assets under management of these startups have increased from $2.3 billion in 2013 to $20 billion in the first quarter of 2017. In Europe, the number of assets currently managed by robo-advisors is not publicly available, but it is said that the total number should be close to 5–6% of that in the US and growing at an equally quick rate. As a result, banks and traditional asset managers are increasingly trying to grasp for footholds through acquisitions and cooperations. For instance, BlackRock acquired in 2015 FutureAdvisor and recently expanded its reach overseas by partnering with a German robo-advisor to distribute its iShares ETFs.

Anika Ley, Media Master Mind

Before and After: Reading 100 ICO projects will make you … (fill in applicable…

Before and After: Reading 100 ICO projects will make you … (fill in applicable: cry/laugh/cringe/angry/rethink the world as we know it)

Crypto arena in 2017 was a real soap opera, composed of really expensive soap. Hundreds of millions worth of soap. It had all the proper ingredients, money, intrigues, lies, hard work, betrayal, government, litigation, public fights, drama and more drama. We fell in love with some projects, we hated the other and with some we just couldn’t decide. But one thing will remain true forever, we were there when it started happening.

Before

Around summer, after a careful consideration, I decided to include ICOs in my research. Having considerable experience with startups and crowdfunding and being entrepreneur myself, I thought there is not much that could caught me off guard. Oh boy (and girl #GenderEquality) how wrong I was.

With my very own version of enthusiasm (read obsession) I started diving into dozens and dozens of ICO projects. Lacking adequate technical background, it was often difficult for me to extrapolate the purpose, functionality and viability of some projects. That did not stop me though. As it apparently did not stop people from investing.

I definitely expected early stage blockchain projects, which included lot of uncertainty, questionable innovation and here and there an attempt to push through something completely absurd. And I got definitely more than I subscribed for.

In between

As a prudent researcher, I picked up a sample of ICOs conducted in the first half of 2017. Few months after their closure we may have a better idea where exactly this is going, at least that was my initial assumption. During that time period, only around 60 ICOs took place, small batch but on the other hand very successful. The likes of Tezos ($202 mil.), TenX ($80 mil.), Status($107 mil.), Bancor($153 mil.) & co. launched their ICO rounds during those months and became instant legends. I have to admit that some of those projects were quite interesting reads. I often caught myself delving into the white papers more than was necessary for the purposes of my research. Besides quite understandable aims of Fintech projects, I discovered also more exotic concepts such as fog computing (SONM), currency backed by labour (Chronobank) or attention-based advertising (Basic Attention Token). One may of course challenge their business viability but as Yoda would say, “creative very they were”. And that’s what I genuinely appreciated. Creative concepts sometimes precede commercialization by months, years or even dozens of years, but that should not prevent inventors from putting ideas out there, regardless of how unrealizable they may sound.

In January 2018, I felt like the ICO landscape was changing so quickly that my initial 2017 ICO batch could no longer suffice for presenting up to date info about the industry. In the end, three months in the real world count for one year in crypto “Matrix” world. New projects were popping up faster than one can say “decentralized, immutable, tamper-proof”. And it was again an interesting read but from a different angle. I browsed through approximately 100 projects, which launched or pre-ICOed in January/February 2018.

The whole endeavor required me to spend long evenings reading, researching, googling and sometimes even chatting with hopefully real people-representatives of the ICO projects that were supposed to answer questions of nosy potential token-buyers. With its ups and downs it left me emotionally exhausted. I will reserve all the graphs and pie charts for my upcoming article but I thought that I could already provide you with a glimpse of my general findings.

After

As a researcher, this ICO expedition left me definitely baffled. Being around startups for past three or four years, I was very much aware how difficult it is to raise early-stage funding and even more challenging to arrange for a follow-up round. And yet these blockchain startups managed to raise amounts which by far exceeded their needs not only for their early stage but also for years to come.

An ill incentive?

The median raised amount for the projects that I studied was around $15 million, mostly in cryptocurrencies. While the amount per se is not so shocking (remember Filecoin with $257 million), it is far ahead of what any startup would get from business angels or a crowdfunding round in that stage. What stage I am talking about? A stage of development without working minimum viable product, without any customers or revenue. In the Netherlands, startups in this stage of their lifecycle “compete” for pilot phase grants of €25,000–50,000 from the government. Psychologically, the higher amount of funding may reinforce irrational optimism bias of entrepreneurs or trigger money-related tensions in the team. In several cases, I noticed that blockchain projects were endangered due to quarrels among the founders, or a disgruntled founder who left the project after the ICO but on the way out damaged the reputation of the whole team to the maximum possible extent. It goes without saying that it has profound impact on the community of token-holders, who in this situation often opt to “vote with their feet” and drop their tokens on the first possible occasion.

White Papers

While in my 2017 sample, the white papers offered very disparate information and content, the 2018 sample demonstrated significant standardization. I would describe it as follows. On approximately first 20 pages, you present an urgent problem of mankind, be it an low access to finance, scarce environmental resources, greedy intermediaries or something equally disturbing. Next, you announce that you have found the ultimate solution and it has something to do with blockchain. Last but not the least, you prove to be transparent by disclosing how much, when and for what purpose you will be fundraising. Deal is done. Specifically, I noticed that many solutions presented in the white papers already exist online but off-chain. The ICO projects hence fail to explain how and if putting such solution on the blockchain will give them sufficient competitive advantage over already existing products and services. The customer in the end cares only about particular elements of the product like the price, the quality and the ease of use. Aside from avid members of the cypherpunk movement, the decentralization per se is not of such value to most of the average Joes and Janes.

Tokenomics

I have to admit it took me quite a while to understand the purpose and the inner workings of tokens. I believe the “tokenomics” of an ICO project is from the business and investor perspective the most intriguing part. Simultaneously, it is an element of the ICO project, where the founders can apply extensive creativity in designing the token and its interaction with the underlying business model. So what do I mean by tokenomics?

Tokenization of platform businesses is a novelty endemic to the blockchain industry. Every ICO project designs its own ecosystem, where participants engage through tokens. Tokens could be defined as “a unit of value that an organization creates to self-govern its business model, and empower its users to interact with its products, while facilitating the distribution and sharing of rewards and benefits to all of its stakeholders”. (For more extensive explanation see Mougayar 2017) Much of the attention has been focused on the issuance and circulation of tokens. Questions like the initial token valuation, volume of the issue, escrow holdings of tokens for later release focused on the creation of optimal level of token scarcity. However, the more profound question is how the tokens interact with the business model underlying the blockchain project.

Using a real life example usually helps to grasp the inner workings of tokenomics. Take for instance Agrello. Agrello is a smart contract platform, which brings together (i) smart contract developers that deploy templates on the platform, (ii) smart contracts users that can choose a suitable template and execute a contract and (iii) smart contract reviewers, who continuously check and improve existing templates. All network participants of Agrello use a token called Delta. Delta token gives these participants the access to the platform and incentivizes them to act in the prescribed manner. While developers and reviewers receive Delta as a reward for their contribution, the users pay with Delta for the services on the platforms. Delta is a so-called native token, which means that its use is confined to this particular platform. At first glance, implementing a native token as a medium of exchange among platform participants could be seen as too restrictive, since it locks the value and provides one single outlet for its use. One may ask why we just simply don’t use Ether, Ripple or any other widely available cryptocurrency. On the other hand, it reinforces the network effect, as the participants in possession of native tokens are very likely to use the same platform again. Furthermore, the platform participants may decide to sell unused tokens on the crypto-exchanges. The tokens can also serve other purposes within the ecosystem. They may carry (i) governance rights (voting), (ii) capital rights (profit sharing) or (iii) other commercial benefits related to the amount of token-holdings (for instance discounts on services).

Tokens are therefore not just digital vouchers, which you purchase and at your convenience exchange for products or services, (this is the parallel that has often been drawn to explain tokens). Tokens can be used in myriad of ways not only to exchange value among parties but also to steer and incentivize certain behavior and engagement of platform participants. Tokenomics is often underdeveloped in the white papers, simultaneously it is the element, which can make or break the ICO project.

ICO Governance

When I buy Apple shares, I become a shareholder, my role, my rights, my position and legal tools I have are clear and widely accepted. As a token-holder the situation is much more ambiguous. Token-holders are definitely stakeholders, they invest significant funds into the ICO project, yet their standing and rights in the governance are often questionable, even more often non-existent. Several projects included a voting right attached to the token, which gives token-holders partial control over the project, however in terms of execution, it is not entirely clear, if these rights are not only a window-dressing exercise without real impact on the governance of the project. From that perspective we can say that ICO governance is underdeveloped or even broken. Only recently, Vitalik Buterin, founder of the Ethereum, introduced a new model, which implements properties of DAO (decentralized autonomous organization) into the ICO governance. This model, coined DAICO, empowers token-holders to decide over allocation of funds raised in an ICO to the ICO team. Moreover, they have power to terminate the smart contract and return the undistributed funds to the token-holders in proportion to their holdings. It is yet to be seen, if this will bring the very much needed sustainability and transparency into ICO governance.

The ICO adventure/drama/comedy/thriller/horror(?) is not over yet, since I still need to process all the data and collected evidence. But I can already conclude that it generated more questions than answers. Personally, I believe that ICOs are here to stay but the format and context in which they are done has to become more refined, transparent and balanced. For now, I will continue my research inquiry into ICO projects, governance and investors. If you have ever invested in at least one ICO, help me grow my data set by filling in this short anonymous questionnaire.

“I worked with startups and I survived!” What it is like to be an intern at ehvLINC Legal & Tax Incubator

ehvLINC is a unique legal & tax incubator that enables startups to get a proper and affordable legal & tax support. Our special sauce are students, young “almost” lawyers seeking for possibilities to acquire practical knowledge. While our main goal is to help startups with all things legal & tax and help them to grow without headaches, we are also on the mission to create a new generation of entrepreneurial lawyers and tax advisors, ones that understand business models, business strategy, technology and innovation and use this knowledge while advising a client. Ones that have startup spirit, lawtrepreneurs & taxentrepreneurs if you will.

This week one of our current interns, Anika Ley, got to interview one of our former interns, Katerina Pouliou, to hear a little bit more about her experience at ehvLINC. This is the result.

Anika: Ok, so let’s start by you shortly introducing yourself!

Katerina: Ok, so I enrolled in the Law and Technology LLM program at Tilburg University last January and recently graduated. Before that I was a trainee lawyer back in Greece, where I come from, and had been admitted to the Bar Association of Thessaloniki. During my first semester in the LLM, I decided to apply to ehvLINC, where I was appointed as a trainee to ATO-GEAR, a start-up based in Eindhoven. I had to draft an IP strategy for the company, as well as review their privacy policies in order for them to be in compliance with the upcoming EU data protection legislation.

Anika: So what motivated you to join the program when you arrived to Tilburg?

Katerina: I wanted to practically implement all the knowledge that I acquired through the program. That way I would be able to not only understand my courses better, but also identify the differences between theory and practice. The experience of working in a tech company, in a real-life environment with actual responsibilities was definitely a plus too.

Anika: Sounds great! You already mentioned a bit what type of work you got to do during your internship, is there anything else you want to add and could you explain a bit how it all went down?

Katerina: Sure! Well, at first we had a meeting with the CEO of the company where he explained the product they are designing (a cool running app) and the issues where he thought they needed some help with. Along with Edwin, the other student who was working through the program for the same company, we divided the work according to our experience and expertise. We had the freedom to work either from home or in the company’s offices. Everything we drafted was checked by a lawyer, also part of the ehvLINC program, and we then presented them to the CEO. Several meetings followed until the end of the program.

Anika: So you got to work very closely with this startup for the period of your internship. Thinking back, what would you say makes working with startups so interesting?

Katerina: I think that start-up CEOs are really invested in their companies and are usually well aware of what their companies need. Working with start-ups can come with some challenges, as from a legal perspective, you might be faced with all kinds of questions, from the simplest one to the most complicated, and this is what makes it so interesting.

Anika: You say it can be challenging working together with startups. Do you remember what had been one of the biggest challenges you had to face? And at the same time, did you experience anything especially rewarding?

Katerina: As I started the internship while I was still in my first semester, and before I was taught all the courses, I remember having to answer some data protection-related questions before I even knew what data protection is about! What seemed a bit crazy and demanding at first, was actually very rewarding at the end, as I managed to deliver. All the research and studying I did for this reason in the meantime actually helped me a lot when I was taught all the data protection courses in the next semester.

Anika: I see, you seem to have had an overall good experience! Was there anything you maybe disliked about the program?